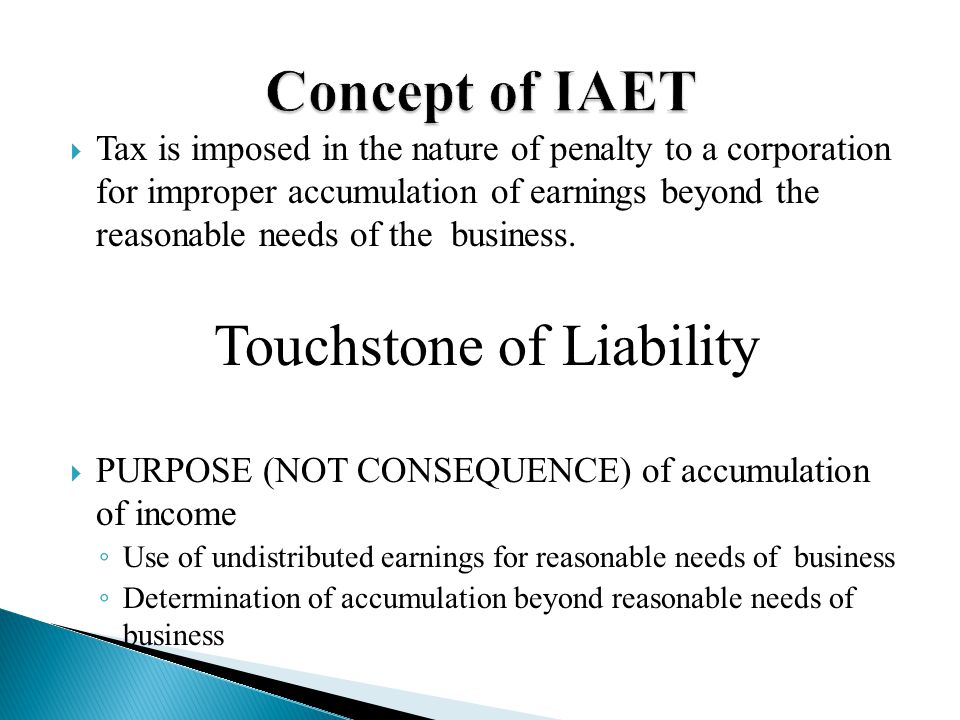

accumulated earnings tax reasonable business needs

The accumulation of reasonable amounts for the payment of reasonably anticipated product liability losses as defined in section 172f as in effect before the date of enactment of the Tax Cuts and Jobs Act as determined under regulations prescribed by the Secretary shall be treated as accumulated for the reasonably anticipated needs of the business. 20 of the rent.

Overview Of Improperly Accumulated Earnings Tax In The Philippines Tax And Accounting Center Inc Tax And Accounting Center Inc

The US tax service considers an amount greater than this amount to exceed reasonable business needs.

. Tax on Accumulated Earnings. If Company A wishes to. Do not keep an accumulated earnings balance that exceeds 250000 or 150000 for personal service corporations What Are Some Examples of Reasonable Business Needs.

Reasonable business needs versus tax avoidance by Machinery and Allied Products Institute 1967 edition in English. If a C corporation retains earnings doesnt distribute them to shareholders above a certain amount an amount which the IRS concludes is beyond the reasonable needs of the business the corporation may be assessed tax penalty called the accumulated earnings tax IRC section 531 equal to 20 percent 15 prior to 2013 of accumulated taxable income. The threshold is 25000 without accumulated earning tax.

The federal government discourages companies from stockpiling their capital by using the accumulated earnings tax. The need to retain earnings and profits. The accumulated earnings tax is a 20 penalty that is imposed when a corporation retains earnings beyond the reasonable needs of its business ie instead of paying dividends with the purpose of avoiding shareholder-level tax seeSec.

ONeill The Accumulated Earnings Tax-Effects of Stock Redemptions 46 TAXES 172 1968. Strategies for Avoiding the Accumulated Earnings Tax. However this opens the door to the Accumulated Earnings Tax AET if profits accumulate beyond the reasonable needs of the business.

The Tax Code defines reasonable needs to include the reasonably anticipated needs of the business. REASONABLE NEEDS OF THE BUSINESS. And profits have been allowed to accumulate beyond the reasonable.

Accumulated earnings can be reduced by dividends actually or deemed paid and corporations are entitled to an accumulated earnings credit which will be the greater of 1 a minimum of a 250000 lifetime credit for most corporations 150000 in the case of a corporation whose principal function is the performance of health legal engineering. An accumulation of the earnings and profits including the undistributed earnings and profits of prior years is in excess of the reasonable needs of the business if it exceeds the amount that a prudent businessman would consider appropriate for the present business purposes and for the reasonably anticipated future needs of the business. The tax is in addition to the.

The primary defense usually levied by the corporation is that the accumulated earnings beyond 25000000 were essential to the reasonable needs of the business. Reasonable business needs include any of the following. Taxable income 350000 federal income tax 119000 dividends.

Accumulated Earnings Tax IRC 531 The purpose of the accumulated earnings tax is to prevent a corporation from accumulating its earnings and. Marjorie corporation accumulated earnings and profits E P at the beginning of 2021 was 210000 including consideration for the dividends listed below Marjorie Corporation also had the following information for 2021. The key term reasonable needs of the business is so subjective in nature that the tax itself is de facto raised by the IRS.

Retain earnings for reasonable business needs and document them in a specific definite and feasibleplan. Needs of the business. Marjorie corporations total reasonable business needs for 2021 was 320000.

The 531 penalty tax is designed to prevent corporations from unreasonably retaining after-tax liquid funds in lieu of paying current dividends to shareholders where they would be again taxed as ordinary income at shareholder tax rates. Percent of the accumulated taxable income in excess of. 1537-2a Income Tax Regs.

This tax was created to discourage companies from withholding profits and paying dividends. 5 1535- 3b 1 ii. The tax rate on accumulated earnings is 20 the maximum rate at which they would be taxed if distributed.

150000 200000 - 100000 250000. When applicable the accumulated earnings tax is levied at the rate of 27y percent of the first 100000 of accumulated taxable income and at. According to the IRS anything above this considered beyond the reasonable needs of the business.

2-2001 includes as among the items which constitutes reasonable needs of the business the allowance for the increase in the accumulation of earnings up to 100 percent of the paid-up capital of the corporation. In periods where corporate tax rates were significantly lower than individual tax rates an obvious incentive existed for. Rudolph Stock Redemptions the Accumulated Earnings Tax-An Update 4 J.

The need to retain earnings and profits. The AET is a penalty tax imposed on corporations for unreasonably accumulating earnings. The accumulated earnings tax equals 396 percent of accumulated taxable income and is in addition to the regular corporate.

The Tax Code defines reasonable needs to include the reasonably anticipated needs of the business. The accumulated earnings tax. Accumulations to Redeem Stock 25 J.

When the revenues or profits are above this level the firm will be subjected to accumulated earnings tax if they do not distribute the dividends to shareholders. If the accumulated taxable income satisfies the reasonable needs test then the accumulated earnings tax will be defeated. This taxadded as a penalty to a companys income tax liabilityspecifically applies to the companys taxable income less the deduction for dividends paid and a standard accumulated tax credit of.

To avoid having to pay for accumulated earnings tax Company A has to distribute at least 100000 of net income as dividends. Polasky Planning for the Disposition of a Substantial Interest in a Closely Held Business 46. The accumulated earnings tax doesnt apply to earnings kept in the business to meet the reasonable needs of the business.

Net Liauid Assets The accumulated earnings and profits of prior years are taken into consideration in determining whether any amount of the earnings and profits of the taxable year has been retained for the reasonable needs of the business. In any proceeding before the Tax Court involving the allegation that a corporation has permitted its earnings and profits to accumulate beyond reasonable business needs the burden of proof is on the Commissioner unless a notification is sent to the taxpayer under IRC 534b However if such a notification is sent to the taxpayer and heshe timely submits the. This is a federal tax levied on businesses that are considered invalid and have above-average incomes.

Learn The Meaning Of Post Trial Balance At Http Www Svtuition Org 2013 07 Post Closing Trial Balance Html Trial Balance Accounting Education Learn Accounting

:max_bytes(150000):strip_icc()/GettyImages-1089395350-f33f180d2b234b268f6df527045f8de0.jpg)

Accumulated Earnings Tax Definition

Doing Business In The United States Federal Tax Issues Pwc

Recognizing And Measuring Tax Benefits From Uncertain Tax Positions

Prepared By Lilybeth A Ganer Revenue Officer Ppt Download

:max_bytes(150000):strip_icc()/GettyImages-1128492098-f6606fdc398b4e0bbecbe4c2fe8493eb.jpg)

Accumulated Earnings Tax Definition

Pin On Saving Money

Corporate Distributions

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download

Avoiding Gain At The S Shareholder Level When A Loan Is Repaid

Does A Company Pay Income Tax On Retained Earnings

Income Tax Computation For Corporate Taxpayers Prepared By

Accounting Cycle Accounting Cycle Learn Accounting Accounting

Understanding The Accumulated Earnings Tax Before Switching To A C Corporation In 2019

Avoiding Gain At The S Shareholder Level When A Loan Is Repaid

/GettyImages-1130199515-b011f8c58a144789b22c7107929ffb8f.jpg)

Accumulated Earnings Tax Definition

Map Pack Rankings Dominate Local Maps Pin Ads Food And Drink Local Map

Benefiting From A Fiscal Tax Year

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download